Global Plant-based Meat Alternatives Market

Plant-based Meat Alternatives Market (Source: Soy, Pea, Wheat, Legumes, and Others (Seeds, Blends, etc.); Product Category: Chicken Alternative, Beef Alternative, Seafood Alternative, Pork Alternative, and Others (Turkey, Lamb, etc.); Product Form: Burgers / Patties, Sausages, Strips & Nuggets, Meatballs, Ground Meat, Shreds & Scrambles, and Others (Slices, Cutlets, etc.); Distribution Channel: Food Retail, HORECA (Hotel/Restaurant/Cafe), and Others) – Global Industry Analysis, Shares, Growth, Trends and Forecast 2021-2036

Categories:

All, Food and Consumer Goods

| Format: PDF/PPT/Excel

| Product ID:

4405

| Report Version:

May 2026

- Report Preview

- Table of Content

- Request Customization

Market Snappshot

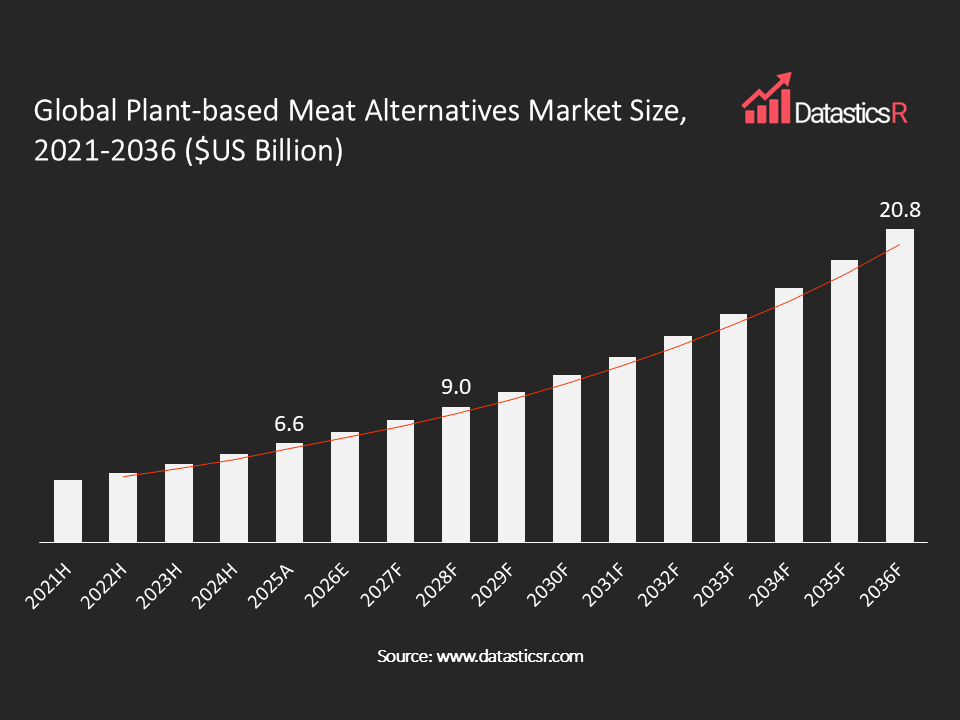

- Market Size in 2025: $US 6.6 Bn

- Forecast Market by 2036: $US 20.8 Bn

- CAGR for the Period 2026-2036: 11%

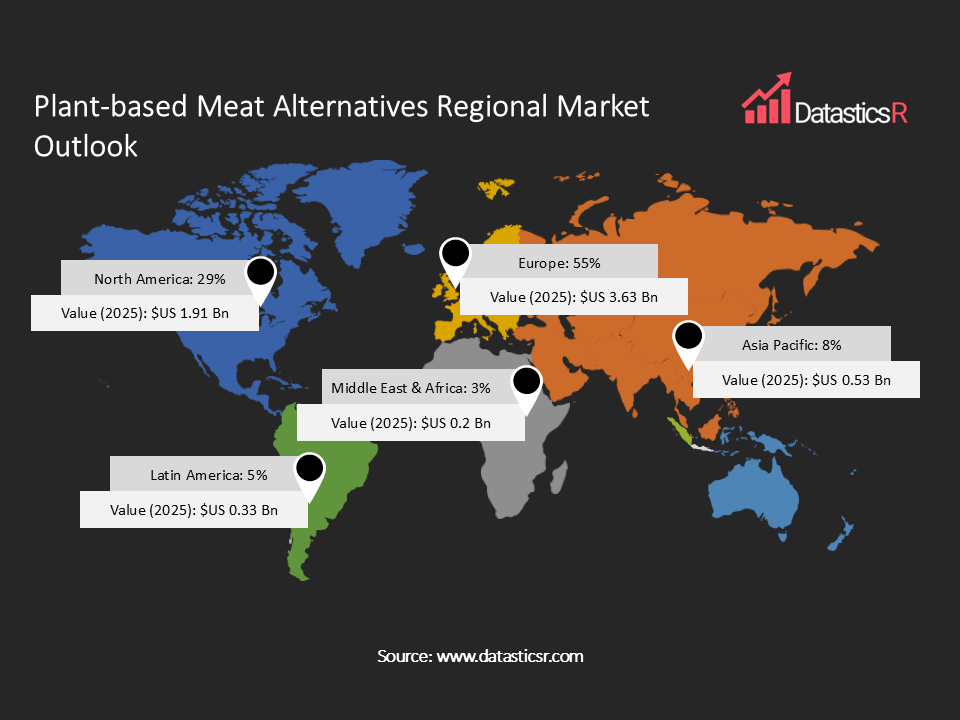

- Top Region in Terms of Market Share: Europe (55%)

- Key Players: Beyond Meat, Field Roast, Conagra Brands (Gardein), Garden Gourmet, Impossible Foods, Kellogg’s (Morningstar), Quorn, Nature´s Richness Holding, Osem Nestle, Heura Foods, MATR Foods, Tyson Foods, Vivera, and Others

Analyst Viewpoint:

The plant-based meat alternative is transitioning beyond its hype phase into a more mature, fundamentals-driven growth cycle; an evolution that is ultimately constructive for investors. The category has progressed from a period of novelty into disciplined commercial execution. Flexitarians now constitute 93% of the plant-based meat consumers in the US, and they all consume meat products as well, which means that this is not a vegan segment but rather one focused on changing consumer preferences within the food segment. Clean label formulations have become a requirement for success, as consumers pay as much attention to ingredients as to nutrition labels. Technologically, the focus is shifting from first generation soy burgers to cleaner labels, better nutrition and extrusion/post processing upgrades that improve texture while controlling cost. In terms of innovations, precision fermentation, high moisture extrusion, and mycoprotein fiber formulations are set to converge in closing the flavor and texture gap with animal proteins. Food service, on the other hand, has shown itself to be the true catalyst for product.

Plant-based Meat Alternatives Market Overview:

Plant-based meats, sometimes referred to as meat analogues or meat substitutes, are products designed to mimic animal-based meat counterparts in flavor, texture, aesthetics, and nutritional composition. Ingredients include proteins from soy, pea, wheat gluten, mycoprotein, fava beans, chickpeas and other sources as well as precision fermentation and mushroom-derived ingredients. Animal agriculture is replaced with alternative protein sources in order to consume protein. Plant-based proteins create 30%-90% less GHG emissions. Institutional food buyers are incorporating ESG goals into their purchasing requirements. Additionally, alternative meats have come a long way from being a niche health food. Certain products on the market today provide more fiber and bioavailable iron than their animal-based counterparts while limiting saturated fats. High moisture extrusion is now the primary method of production versus traditional dry extrusion to create fibrous, meat-like structures. Newer technologies such as wet spinning and shear cell allow for whole-cut analogues such as steak, fillets, and shredded applications. Fermentation is being used to deepen umami flavor profiles as well as reduce any unwanted plant aftertastes. While the technology to create these meats has improved, the cost of production for alt-proteins is still on higher side. With that said, companies in the space are trying to decrease the cost of ingredients by controlling more of the supply chain, developing contract-growing and blending multiple proteins to hit price parity in near future.

| Drivers | Rapid Flexitarian Shift and Meat‑Reduction Behavior Reshaping Demand in Europe, North America and Beyond |

| Foodservice Operators Embedding Plant-Based Proteins Permanently in Core Menus |

Rapid Flexitarian Shift and Meat Reduction Behavior Reshaping Demand in Europe, North America and Beyond

One of the strongest structural enablers is the emergence of flexitarianism and reductionism, especially among consumers in Europe and developed countries. As per current stats, 27% of Europeans are identified as flexitarians, within which Germany and Austria percentages are 40% and 37%, respectively. This means that “less meat” is no longer a niche concept, but a lifestyle option widely adopted by individuals across Europe.

According to another survey on consumers in the US, it has been found that 57% of plant-based meat-eaters are classified as omnivores, whereas only 11% belong to vegetarians, pescatarians, or vegans category. Therefore, it is evident that the target customer is more inclined towards being a flexitarian meat-eater rather than converting entirely into plant-based meat products. From a business perspective, these customers compare plant-based meat products like burgers and sausages on the same basis as traditional animal meat in terms of taste, price, and versatility. In the past ten years, retail sales of plant-based meats have multiplied nearly three times in the US.

Market players benefit from the shift towards flexitarianism in terms of strategies other than those related to meat alternatives alone. For instance, manufacturers of plant-based products such as milk, yogurt, cheese, and meals can offer a package of flexitarian options. Similarly, manufacturers of ingredients can create a protein-based formulation system that could be used in the manufacture of meat, dairy, and meals. This favorable shift in consumer preferences is expected to unlock significant growth opportunities over the forecast period.

According to another survey on consumers in the US, it has been found that 57% of plant-based meat-eaters are classified as omnivores, whereas only 11% belong to vegetarians, pescatarians, or vegans category. Therefore, it is evident that the target customer is more inclined towards being a flexitarian meat-eater rather than converting entirely into plant-based meat products. From a business perspective, these customers compare plant-based meat products like burgers and sausages on the same basis as traditional animal meat in terms of taste, price, and versatility. In the past ten years, retail sales of plant-based meats have multiplied nearly three times in the US.

Market players benefit from the shift towards flexitarianism in terms of strategies other than those related to meat alternatives alone. For instance, manufacturers of plant-based products such as milk, yogurt, cheese, and meals can offer a package of flexitarian options. Similarly, manufacturers of ingredients can create a protein-based formulation system that could be used in the manufacture of meat, dairy, and meals. This favorable shift in consumer preferences is expected to unlock significant growth opportunities over the forecast period.

Foodservice Operators Embedding Plant-Based Proteins Permanently in Core Menus

The single largest factor, which has been overlooked within this industry, is not related to retail shelf expansion but to the permanency of foodservice menus. The fast-food companies showing inclination towards plant-based meat alternatives on their menu, this means that they will need to consider their needs for supply and plan ahead, train employees, and ensure logistics. This difference between promotion and operation has a huge impact on the signal that is being sent to manufacturing companies. Plant-based products are already available permanently in large fast-food chains across North America, Europe, and Asia Pacific, in addition to university canteens, hospitals, airlines, and office cafeterias, due to sustainability initiatives.

Impact-wise, this is huge. Although foodservice represents only a quarter of plant-based meat volume in advanced economies today, it outsizes itself when it comes to trial and repurchase rates. People who sample a plant-based patty through foodservice are more likely to buy one from retailers down the road. Foodservice becomes a way of acquiring consumers rather than merely generating sales. Moreover, chefs using plant-based products are providing instant feedback on the taste profile, which can be integrated into product formulations quicker than regular consumer feedback studies. This is why brands such as Impossible Foods and Beyond Meat have invested heavily in expanding their foodservice sales capabilities.

The trend toward institutional purchasing is growing in Europe & the U.S. This trend moves slowly but provides a very stable driver of demand, one that will be extremely difficult to displace once implemented.

Impact-wise, this is huge. Although foodservice represents only a quarter of plant-based meat volume in advanced economies today, it outsizes itself when it comes to trial and repurchase rates. People who sample a plant-based patty through foodservice are more likely to buy one from retailers down the road. Foodservice becomes a way of acquiring consumers rather than merely generating sales. Moreover, chefs using plant-based products are providing instant feedback on the taste profile, which can be integrated into product formulations quicker than regular consumer feedback studies. This is why brands such as Impossible Foods and Beyond Meat have invested heavily in expanding their foodservice sales capabilities.

The trend toward institutional purchasing is growing in Europe & the U.S. This trend moves slowly but provides a very stable driver of demand, one that will be extremely difficult to displace once implemented.

Plant-based Meat Alternatives Regional Market Outlook:

Europe dominates global market share with 55% in retail sales, reflecting high per‑capita consumption and a structurally larger flexitarian base. Nearly 1/4th of Europeans identifies as flexitarian, with Germany, Austria and the Netherlands showing particularly strong meat‑reduction trends, which translates into strong retail rotation for burgers, mince, and schnitzel‑style products.

North America ranks second in global market, with estimates indicating around 29% of global sales in 2025, supported by strong brand recognition, extensive retail distribution, and entrenched QSR partnerships.

Asia Pacific is a high‑growth region, leveraging long traditions of soy and wheat protein, rapid urbanization, and the rise of modern retail; plant-based milk is already strong across the region, providing a route to cross‑sell meat analogues as price points normalize.

In the Middle East & Africa, demand is emerging through modern grocery, health‑conscious urban consumers, and tourism‑driven foodservice hubs, often focusing on burger, shawarma and kebab analogues positioned as premium Western or fusion concepts, while Latin America is seeing momentum in Brazil, Mexico, and Chile where global and regional brands are partnering with retailers and QSR chains, using plant-based burgers, sausages, and empanada fillings to tap into familiar local dishes while addressing health and sustainability concerns.

North America ranks second in global market, with estimates indicating around 29% of global sales in 2025, supported by strong brand recognition, extensive retail distribution, and entrenched QSR partnerships.

Asia Pacific is a high‑growth region, leveraging long traditions of soy and wheat protein, rapid urbanization, and the rise of modern retail; plant-based milk is already strong across the region, providing a route to cross‑sell meat analogues as price points normalize.

In the Middle East & Africa, demand is emerging through modern grocery, health‑conscious urban consumers, and tourism‑driven foodservice hubs, often focusing on burger, shawarma and kebab analogues positioned as premium Western or fusion concepts, while Latin America is seeing momentum in Brazil, Mexico, and Chile where global and regional brands are partnering with retailers and QSR chains, using plant-based burgers, sausages, and empanada fillings to tap into familiar local dishes while addressing health and sustainability concerns.

Key Companies in Plant-based Meat Alternatives Market:

There are only a few major competitors, such as Beyond Meat, Impossible Foods, etc., who are still driving innovation in the global industry of plant-based meat. On the other hand, there are many other competitors emerging in the mid-level market that are using existing food companies’ (Tyson Foods, Conagra Brands, etc.) wide network of distribution channels to grow rapidly in the market. The early innovators are trying to develop new ingredients and reduce costs of production while the major food companies are concentrating on expanding their reach via retail channels and collaborations with restaurants.

The key players of the market are Beyond Meat, Field Roast, Conagra Brands (Gardein), Garden Gourmet, Impossible Foods, Kellogg’s (Morningstar), Quorn, Nature´s Richness Holding, Osem Nestle, Heura Foods, MATR Foods, Tyson Foods, Vivera, and Others.

The key players of the market are Beyond Meat, Field Roast, Conagra Brands (Gardein), Garden Gourmet, Impossible Foods, Kellogg’s (Morningstar), Quorn, Nature´s Richness Holding, Osem Nestle, Heura Foods, MATR Foods, Tyson Foods, Vivera, and Others.

Key Developments in Plant-based Meat Alternatives Market:

| 1. Grill’d, Beyond Meat partner to launch new plant-based offering: In August 2025, Grill’d collaborated with plant-based meat brand Beyond Meat to launch the latest version of the Beyond Burger, called the Beyond Burger IV. The new fourth-generation Beyond Burger is free from soy, gluten, and GMOs and is now cooked with avocado oil. |

| 2. JBS acquiring The Vegetarian Butcher from Unilever: In March 2025, Vivera, a subsidiary of JBS SA, one of the world’s largest meat processors, is acquiring The Vegetarian Butcher from Unilever. The Vegetarian Butcher sells a variety of plant-based meat alternative applications to retailers and foodservice operators in 55 markets around the world. |

Plant-based Meat Alternatives Market Attributes:

| ATTRIBUTE | DETAILS |

| Market Value, 2025 | $US 6.60 Billion |

| Forecasted Market Value, 2036 | $US 20.80 Billion |

| CAGR (2026-2036) | 11% |

| Analysis Period | 2021-2036 |

| Historic Period | 2021-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2036 |

| Volume Unit | Ton |

| Value Unit | $US Billion |

| Market Segmentation | By Source

By Product Category

By Product Form

By Distribution Channel

By Region

|

| Companies Profiles |

|

| Customization Request | Available upon request |

1. Introduction

1.1. Report Scope

1.2. Market Segmentations and Definitions

1.3. Geographical Coverage

2. Executive Summary

2.1. Key Facts and Figures

2.2. Trends Impacting the Market

2.3. DatasticsR Growth Opportunity Matrix

3. Market Overview

3.1. Global Plant-based Meat Alternatives Market Analysis and Forecast, 2021-2036

3.1.1. Global Plant-based Meat Alternatives Market Size (Tons)

3.1.2. Global Plant-based Meat Alternatives Market Size ($US Bn)

3.2. Supply-side and Demand-side Trends

3.3. Technology Roadmap and Developments

3.4. Market Dynamics

3.4.1. Drivers

3.4.2. Restraints

3.4.3. Opportunities

3.5. Porter’s Five Forces Analysis

3.6. PESTL Analysis

3.7. Industry SWOT Analysis

3.8. Regulatory Landscape

3.9. Value Chain Analysis

3.9.1. List of Raw Material Suppliers

3.9.2. List of Manufacturing Companies

3.9.3. List of Dealers/Distributors

3.9.4. List of Potential Customers

3.10. Impact of Current Geopolitical Scenario on the Market

4. Technical Analysis

4.1. Product Specification Analysis

4.2. Details of Production Distribution Channel

4.3. Technology Adoption and Emerging Technologies

4.4. R&D Trends and Patents Landscape

4.5. Cost Structure and Profitability Analysis

5. Global Production Output Analysis (Tons), by Region, 2025

5.1. North America

5.2. Europe

5.3. Asia Pacific

5.4. Latin America

5.5. Middle East and Africa

6. Import-export Analysis Volume (Tons) and Value ($US Bn), by Key Country, 2021-2025

7. Price Trend Analysis and Forecasting ($US/Ton), 2021-2036

7.1. Price Trend Analysis and Forecasting, by Product Category

7.2. Price Trend Analysis and Forecasting, by Region

8. Global Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

9. Global Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

10. Global Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

11. Global Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

12. Global Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Region, 2021-2036

13. North America Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

14. North America Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

15. North America Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

16. North America Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

17. U.S. Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

18. U.S. Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

19. U.S. Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

20. U.S. Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

21. Canada Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

22. Canada Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

23. Canada Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

24. Canada Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

25. Europe Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

26. Europe Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

27. Europe Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

28. Europe Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

29. Germany Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

30. Germany Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

31. Germany Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

32. Germany Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

33. Austria Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

34. Austria Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

35. Austria Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

36. Austria Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

37. Netherlands Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

38. Netherlands Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

39. Netherlands Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

40. Netherlands Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

41. U.K. Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

42. U.K. Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

43. U.K. Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

44. U.K. Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

45. France Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

46. France Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

47. France Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

48. France Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

49. Italy Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

50. Italy Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

51. Italy Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

52. Italy Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

53. Spain Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

54. Spain Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

55. Spain Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

56. Spain Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

57. Russia & CIS Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

58. Russia & CIS Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

59. Russia & CIS Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

60. Russia & CIS Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

61. Rest of Europe Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

62. Rest of Europe Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

63. Rest of Europe Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

64. Rest of Europe Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

65. Asia Pacific Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

66. Asia Pacific Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

67. Asia Pacific Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

68. Asia Pacific Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

69. China Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

70. China Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

71. China Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

72. China Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

73. India Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

74. India Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

75. India Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

76. India Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

77. Japan Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

78. Japan Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

79. Japan Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

80. Japan Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

81. South Korea Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

82. South Korea Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

83. South Korea Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

84. South Korea Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

85. Taiwan Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

86. Taiwan Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

87. Taiwan Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

88. Taiwan Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

89. Australia Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

90. Australia Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

91. Australia Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

92. Australia Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

93. ASEAN Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

94. ASEAN Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

95. ASEAN Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

96. ASEAN Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

97. Rest of Asia Pacific Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

98. Rest of Asia Pacific Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

99. Rest of Asia Pacific Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

100. Rest of Asia Pacific Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

101. Latin America Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

102. Latin America Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

103. Latin America Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

104. Latin America Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

105. Brazil Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

106. Brazil Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

107. Brazil Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

108. Brazil Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

109. Mexico Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

110. Mexico Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

111. Mexico Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

112. Mexico Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

113. Chile Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

114. Chile Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

115. Chile Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

116. Chile Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

117. Argentina Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

118. Argentina Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

119. Argentina Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

120. Argentina Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

121. Rest of Latin America Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

122. Rest of Latin America Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

123. Rest of Latin America Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

124. Rest of Latin America Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

125. Middle East & Africa Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

126. Middle East & Africa Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

127. Middle East & Africa Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

128. Middle East & Africa Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

129. Saudi Arabia Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

130. Saudi Arabia Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

131. Saudi Arabia Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

132. Saudi Arabia Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

133. UAE Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

134. UAE Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

135. UAE Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

136. UAE Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

137. South Africa Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

138. South Africa Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

139. South Africa Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

140. South Africa Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

141. Rest of Middle East & Africa Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Source, 2021-2036

142. Rest of Middle East & Africa Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Category, 2021-2036

143. Rest of Middle East & Africa Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Product Form, 2021-2036

144. Rest of Middle East & Africa Plant-based Meat Alternatives Market Analysis and Forecasting (Tons) ($US Bn), by Distribution Channel, 2021-2036

145. Competition Landscape

145.1. Market Share Analysis (%), by Company, 2025

145.2. Competitive Benchmarking

145.3. Company Profiles

145.3.1. Beyond Meat

145.3.1.1. Company Overview

145.3.1.2. Product Portfolio

145.3.1.3. Financials

145.3.1.4. Geographical Footprint

145.3.1.5. SWOT Analysis

145.3.1.6. Recent Developments and Strategies

145.3.2. Field Roast

145.3.2.1. Company Overview

145.3.2.2. Product Portfolio

145.3.2.3. Financials

145.3.2.4. Geographical Footprint

145.3.2.5. SWOT Analysis

145.3.2.6. Recent Developments and Strategies

145.3.3. Conagra Brands (Gardein)

145.3.3.1. Company Overview

145.3.3.2. Product Portfolio

145.3.3.3. Financials

145.3.3.4. Geographical Footprint

145.3.3.5. SWOT Analysis

145.3.3.6. Recent Developments and Strategies

145.3.4. Garden Gourmet

145.3.4.1. Company Overview

145.3.4.2. Product Portfolio

145.3.4.3. Financials

145.3.4.4. Geographical Footprint

145.3.4.5. SWOT Analysis

145.3.4.6. Recent Developments and Strategies

145.3.5. Impossible Foods

145.3.5.1. Company Overview

145.3.5.2. Product Portfolio

145.3.5.3. Financials

145.3.5.4. Geographical Footprint

145.3.5.5. SWOT Analysis

145.3.5.6. Recent Developments and Strategies

145.3.6. Kellogg’s (Morningstar)

145.3.6.1. Company Overview

145.3.6.2. Product Portfolio

145.3.6.3. Financials

145.3.6.4. Geographical Footprint

145.3.6.5. SWOT Analysis

145.3.6.6. Recent Developments and Strategies

145.3.7. Quorn

145.3.7.1. Company Overview

145.3.7.2. Product Portfolio

145.3.7.3. Financials

145.3.7.4. Geographical Footprint

145.3.7.5. SWOT Analysis

145.3.7.6. Recent Developments and Strategies

145.3.8. Nature´s Richness Holding GmbH

145.3.8.1. Company Overview

145.3.8.2. Product Portfolio

145.3.8.3. Financials

145.3.8.4. Geographical Footprint

145.3.8.5. SWOT Analysis

145.3.8.6. Recent Developments and Strategies

145.3.9. Osem Nestle

145.3.9.1. Company Overview

145.3.9.2. Product Portfolio

145.3.9.3. Financials

145.3.9.4. Geographical Footprint

145.3.9.5. SWOT Analysis

145.3.9.6. Recent Developments and Strategies

145.3.10. Heura Foods

145.3.10.1. Company Overview

145.3.10.2. Product Portfolio

145.3.10.3. Financials

145.3.10.4. Geographical Footprint

145.3.10.5. SWOT Analysis

145.3.10.6. Recent Developments and Strategies

145.3.11. MATR Foods

145.3.11.1. Company Overview

145.3.11.2. Product Portfolio

145.3.11.3. Financials

145.3.11.4. Geographical Footprint

145.3.11.5. SWOT Analysis

145.3.11.6. Recent Developments and Strategies

145.3.12. Tyson Foods

145.3.12.1. Company Overview

145.3.12.2. Product Portfolio

145.3.12.3. Financials

145.3.12.4. Geographical Footprint

145.3.12.5. SWOT Analysis

145.3.12.6. Recent Developments and Strategies

145.3.13. Vivera

145.3.13.1. Company Overview

145.3.13.2. Product Portfolio

145.3.13.3. Financials

145.3.13.4. Geographical Footprint

145.3.13.5. SWOT Analysis

145.3.13.6. Recent Developments and Strategies

145.3.14. Others

146. Appendix

- Get Started -

Get insights that lead to new growth opportunities

- Talk to Experts -

Get answers to your queries on this report from our experts

Frequently Asked Questions

The global Plant-based Meat Alternatives market in 2025 was $US 6.60 Billion.

The global Plant-based Meat Alternatives market will be $US 20.80 Billion by 2036.

The expected growth rate (CAGR%) of the global Plant-based Meat Alternatives market is 11% for the period 2026-2036.

Rapid flexitarian shift and meat reduction behavior reshaping demand in Europe, North America and beyond. And Foodservice operators embedding plant-based proteins permanently in core menus.

Plant-based Beef Alternative was the largest consuming segment among all in Plant-based Meat Alternatives Market in 2025.

Europe was the leading regions for Plant-based Meat Alternatives holding around 55% of the global market in 2025.

Beyond Meat, Field Roast, Conagra Brands (Gardein), Garden Gourmet, Impossible Foods, Kellogg’s (Morningstar), Quorn, Nature´s Richness Holding, Osem Nestle, Heura Foods, MATR Foods, Tyson Foods, Vivera, and Others.