Medical Polycarbonate Market

Medical Polycarbonate Market (Grade – Standard Grade, Heat Resistant Grade, Optical Grade, Lipid Resistant Grade, and Others; Processing Method – Injection Molding, Extrusion, Blow Molding, Thermoforming, and Others; Application; and End-Use Industry) – Global Industry Analysis, Shares, Growth, Trends and Forecast 2020-2035

Categories:

All, Chemicals and Materials, Healthcare and Life Sciences

| Format: PDF/PPT/Excel

| Product ID:

3815

| Report Version:

August

- Report Preview

- Table of Content

- Request Customization

Market Snappshot

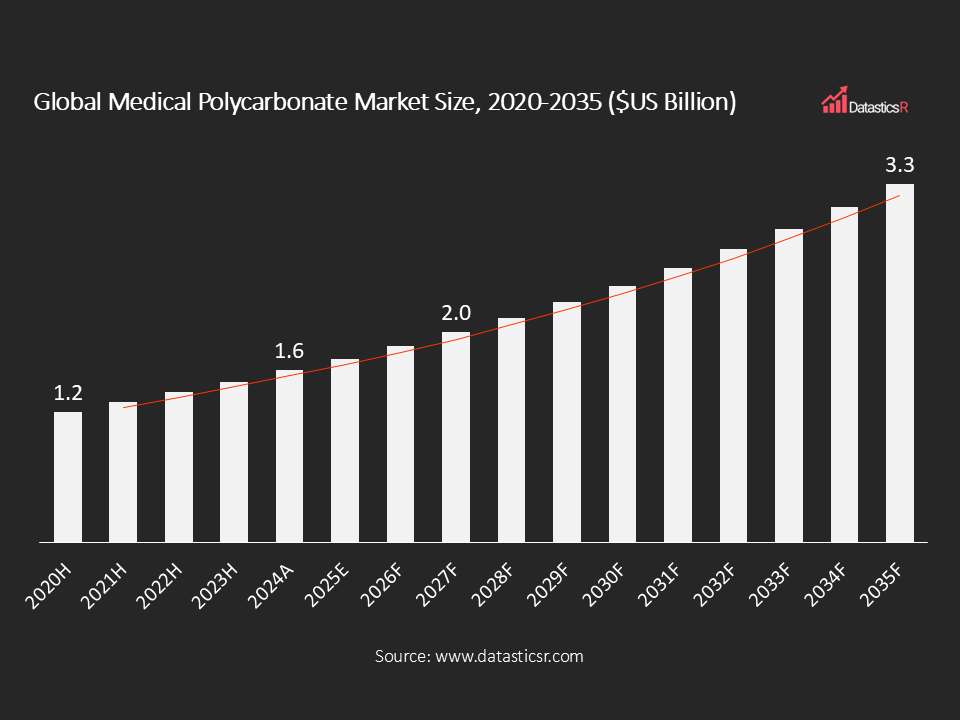

- Market Size in 2024: $US 1.6 Billion

- Forecast Market by 2035: $US 3.3 Billion

- CAGR for the Period 2025-2035: 6.9%

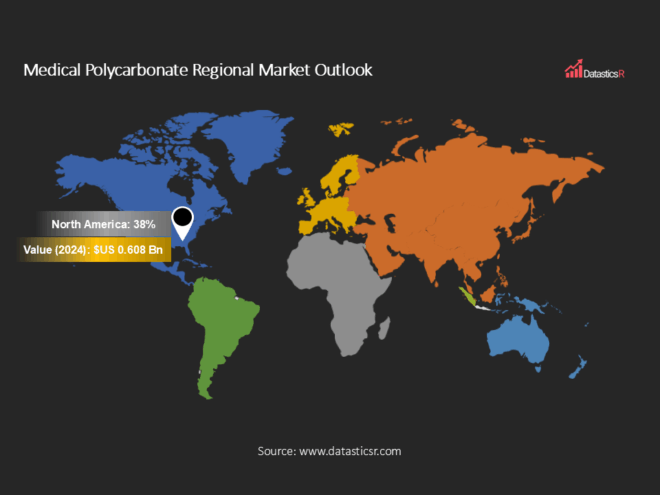

- Top Region in Terms of Market Share: Asia Pacific (38%)

- Key Players: Covestro AG, SABIC, Teijin Limited, Trinseo S.A., Mitsubishi Chemical/Engineering-Plastics, Lotte Chemical, BASF, CHIMEI Corporation, Trinseo, and Others.

Analyst Viewpoint:

Medical-grade polycarbonate continues to be a strategic material for makers of medical devices due to its unique combination of optical clarity, impact strength, tolerance to sterilization, and processing ease. Demand is being driven by expansion in single-use devices, housings for diagnostic instruments, and small drug-delivery systems that demand clear, rugged, and biocompatible components. Regulatory focus on sterilizability (autoclave, gamma, EtO) and infection control fuels usage of high-heat and disinfectant-resistant PC grades, while OEMs require grades with low carbon footprint and recyclability. Supply-side trends are the deep-pockets petrochemical/polymer majors placing strategic investments in focused medical portfolios and capacity increases to capture qualification cycles for device OEMs.

Challenges are rigorous medical approvals, qualification times that are very long, and commodity PC supplier price pressure. Technology development including copolymer alloys, antimicrobial modifiers, low-extractables grades and HC-compliant low-CO₂ solutions is expanding applications to wearable devices and connected diagnostics, enabling consistent, mid-single-digit CAGR throughout the coming decade.

Medical Polycarbonate Market Overview:

Medical polycarbonate (PC) is an engineering thermoplastic that is specifically formulated and processed to satisfy medical-industry needs (biocompatibility, resistance to sterilization, low extractables, clarity, and dimensional stability). In terms of its functions, medical PC finds application in clear housings, syringes and drug delivery parts, fluidics connectors, diagnostic optics, covers and screens, and engineered structural components in single-use and reusable devices. Manufacturing pathways are extrusion to create sheet/film for displays and packaging, injection molding for intricate, thin-wall components, and compounding for specialty masterbatch incorporation (antimicrobial, flame retardant, colorants). Technologies in production are changing, producers supply specialized medical PC grades (heat-resistant and extractable-low grades polycarbonates) and extend certification (USP, ISO 10993 biocompatibility).

Main production challenges are strict quality systems (ISO 13485 traceability), extractables/leachable control, and OEM validation qualification timelines, which create entry barriers but also enable premium pricing. Industry development involves cross-industry co-operation (material suppliers co-operating with device OEMs to speed part validation), sustainability initiatives (low-CO₂ and recycled-content medical PC where applicable), and product innovations (enhanced sterilization durability and chemical resistance to disinfectants). Statistically, the wider medical plastics/medical device materials market is growing as the international medical device market expands and aging populations drive device demand. Medical-grade PC takes an increasing percentage where transparency, impact resistance and sterilization capability are paramount.

| Drivers | Growing Aging Populations Worldwide, Coupled with Rising Procedural Volumes, are Fueling Demand for Medical Devices |

| Increase need for Sterilizable, Transparent, Durable Polymers and Regulatory Compliance |

Growing Aging Populations Worldwide, Coupled with Rising Procedural Volumes, are Fueling Demand for Medical Devices

Demographic transition to an aging population continues unabated, with both advanced as well as developing economies experiencing a steep improvement in life expectancy. This trend pushes directly the use of diagnostic imaging, minimally invasive procedure, orthopedic implants, cardiovascular stents, and home healthcare solutions. All of these uses rely significantly on materials capable of balancing transparency, safety, impact resistance, and regulatory approval, where medical-grade polycarbonate stands out. Other than aging, life-threatening diseases such as diabetes, cancer, and cardiovascular diseases are on the rise, further boosting demand for advanced medical devices.

2024 and 2025 healthcare systems seek to relieve hospital pressure through home-based monitoring and wearable diagnostics, also in line with the application of polycarbonate for weight-saving, ergonomic, and toughened device parts. OEMs are also scaling up production of single-use device and drug delivery systems to accommodate increasing procedural volumes, particularly in geographies with emerging healthcare infrastructure. This offers resin suppliers not just opportunities for bulk supply but also opportunities for co-development of customized grades for specific device segments. The action also encourages investment in supply chain security, with OEMs clamoring for long-term reliability and certification assistance. Overall, the increasing healthcare cost burden of aging populations testifies to medical polycarbonate’s significant position, promising consistent demand among devices that balance clinical effectiveness and patient comfort.

Increase Need for Sterilizable, Transparent, Durable Polymers and Regulatory Compliance

Sterility and safety are strict in the medicine, the demand for more aggressive infection and disinfection control processes that still remain on controlling the choice of materials. Polycarbonate of medical grade is now among the most common polymers being used in an attempt to meet the demands since it may be subjected to repeated autoclave, ethylene oxide, gamma radiation, and hydrogen peroxide plasma sterilization cycles. The toughness, chemical resistance, and high transparency of polycarbonate are what manufacturers rely upon to provide safe and reliable performance as reusable surgical instruments, syringe cartridges, or diagnostic cartridges.Regulatory needs have converged in, with global regulators more and more placing emphasis on biocompatibility testing, extractables/leachable testing, and long-term resistance under harsh sterilant. ISO 10993 standards and FDA device guidance documents remain the standards to which manufacturers must comply. For suppliers, it is both a curse and a blessing: qualification processes are costly, typically taking years to generate data, but once qualified, they establish a long-lasting moat for stable products. In 2024, suppliers are also creating low-extractable and disinfectant-resistant formulations to aid growing demand for reusable medical devices and device design driven by environmental concerns.Commercially, the reliability of compliant and sterilizable materials reduces the cost of healthcare by decreasing device failure and patient risk. With hospitals and OEMs calling for certifiable supply chains, resin manufacturers are developing dedicated medical portfolios and funding application-testing facilities. This makes medical polycarbonate more than a raw material but as value-adding compliance, safety, and innovation enabler throughout the changing landscape of medical technology.

Medical Polycarbonate Regional Market Outlook:

North America dominates the market with 38% share because of its big medical device sector, high per-capita healthcare expenditure, and a robust adoption of advanced diagnostics & disposable devices, and investments by suppliers and proximity to the OEMs ensure large deals.

Europe is second largest market where demand is fueled by hospitals, advanced diagnostics, and regulatory stringency; sustainability and circularity policies are inducing low-carbon and certified material adoption.

Asia Pacific records highest CAGR owing to increasing healthcare infrastructure, increasing surgical volumes, and domestic device manufacturing (China, India, Japan, South Korea). APAC also experiences increasing domestic polymer production and capacity additions.

Middle East & Africa, smaller base but growing investments in the private healthcare clinics and diagnostic centers underpin the niche adoption.

In Latin America, selective urban areas lead moderate growth, import-reliant device markets, and sustained upticks in local production.

Key Companies in Medical Polycarbonate Market:

Mass chemical and specialty resin players control medical polycarbonate supply owing to technical and regulatory requirements of device original equipment manufacturers (OEMs). Specialty-oriented medical portfolios, R&D in low-extractables, and phased capacity increments or focused product introduction are utilized by market leaders to gain faster OEM qualification. Competitive strategies include co-development with device companies, offering medical-grade certification assistance, and launching specialty grades (heat-resistance, disinfectant-resistance, low-CO₂). Merger, geographically positioned additions, and product differentiation (antimicrobial, recycled content) are common tactical responses.Covestro AG, SABIC, Teijin Limited, Trinseo S.A., Mitsubishi Chemical/Engineering-Plastics, Lotte Chemical, BASF, CHIMEI Corporation, Trinseo, Wanhua Chemical, Idemitsu Kosan, Eastman, GOEX Corporation, Luxi Chemical, RTP Company, and others are major operating in this market.

Key Developments in Medical Polycarbonate Market:

| 1. Covestro expands low-carbon & high-heat medical PC portfolio: In February 2025, Covestro launched and expanded its Makrolon and Apec medical-grade polycarbonates, offering heat-stable, disinfection-resistant, and low-CO₂ versions that are tailored for stringent sterilization and sustainability requirements. |

| 2. Deepak Chem Tech invests Rs 5,000 crore to expand polycarbonate production: In November 2024, Deepak Chem Tech Limited announced a Rs 5,000 crore investment in the construction of a 165,000 MT/year polycarbonate facility at Dahej, Gujarat. From Trinseo assets acquisition and CALIBR tech licensing, the growth in the focused on automotive, electronics, medical devices, and aerospace applications has made it more dominant in the high-performance engineering polymers. |

Medical Polycarbonate Market Attributes:

| ATTRIBUTE | DETAILS |

| Market Value, 2024 | $US 1.6 billion |

| Forecasted Market Value, 2035 | $US 3.3 billion |

| CAGR (2025-2035) | 6.9% |

| Analysis Period | 2025-2035 |

| Historic Period | 2020-2023 |

| Base Year | 2024 |

| Forecast Period | 2025-2035 |

| Volume Unit | Tons |

| Value Unit | $US billion |

| Market Segmentation | By Grade

By Processing Method

By Application

By End-use

By Region

|

| Companies Profiles |

|

| Customization Request | Available upon request |

1. Introduction

1.1. Report Scope

1.2. Market Segmentations and Definitions

1.3. Geographical Coverage

2. Executive Summary

2.1. Key Facts and Figures

2.2. Trends Impacting the Market

2.3. DatasticsR Growth Opportunity Matrix

3. Market Overview

3.1. Global Medical Polycarbonate Market Analysis and Forecast, 2020-2035

3.1.1. Global Medical Polycarbonate Market Size (Tons)

3.1.2. Global Medical Polycarbonate Market Size ($US Bn)

3.2. Supply-side and Demand-side Trends

3.3. Technology Roadmap and Developments

3.4. Market Dynamics

3.4.1. Drivers

3.4.2. Restraints

3.4.3. Opportunities

3.5. Porter’s Five Forces Analysis

3.6. PESTL Analysis

3.7. Industry SWOT Analysis

3.8. Regulatory Landscape

3.9. Value Chain Analysis

3.9.1. List of Raw Material Suppliers

3.9.2. List of Manufacturers

3.9.3. List of Dealers/Distributors

3.9.4. List of Potential Customers

3.10. Impact of Current Geopolitical Scenario on the Market

4. Technical Analysis

4.1. Product Specification Analysis

4.2. Details of Application

4.3. Technology Adoption and Emerging Technologies

4.4. R&D Trends and Patents Landscape

4.5. Cost Structure and Profitability Analysis

5. Global Production Output Analysis (Tons), by Region, 2024

5.1. North America

5.2. Europe

5.3. Asia Pacific

5.4. Latin America

5.5. Middle East and Africa

6. Import-export Analysis Volume (Tons) and Value ($US Bn), by Key Country, 2020-2024

7. Price Trend Analysis and Forecasting ($US/Ton), 2020-2035

7.1. Price Trend Analysis and Forecasting, by Grade

7.2. Price Trend Analysis and Forecasting, by Region

8. Global Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

9. Global Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

10. Global Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

11. Global Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

12. Global Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Region, 2020-2035

13. North America Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

14. North America Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

15. North America Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

16. North America Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

17. U.S. Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

18. U.S. Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

19. U.S. Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

20. U.S. Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

21. Canada Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

22. Canada Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

23. Canada Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

24. Canada Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

25. Europe Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

26. Europe Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

27. Europe Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

28. Europe Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

29. Germany Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

30. Germany Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

31. Germany Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

32. Germany Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

33. U.K. Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

34. U.K. Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

35. U.K. Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

36. U.K. Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

37. France Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

38. France Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

39. France Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

40. France Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

41. Italy Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

42. Italy Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

43. Italy Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

44. Italy Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

45. Spain Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

46. Spain Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

47. Spain Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

48. Spain Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

49. Russia & CIS Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

50. Russia & CIS Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

51. Russia & CIS Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

52. Russia & CIS Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

53. Rest of Europe Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

54. Rest of Europe Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

55. Rest of Europe Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

56. Rest of Europe Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

57. Asia Pacific Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

58. Asia Pacific Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

59. Asia Pacific Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

60. Asia Pacific Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

61. China Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

62. China Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

63. China Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

64. China Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

65. India Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

66. India Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

67. India Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

68. India Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

69. Japan Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

70. Japan Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

71. Japan Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

72. Japan Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

73. South Korea Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

74. South Korea Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

75. South Korea Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

76. South Korea Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

77. Taiwan Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

78. Taiwan Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

79. Taiwan Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Fabrication Technology, 2020-2035

80. Taiwan Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

81. Taiwan Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

82. Australia Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

83. Australia Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

84. Australia Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Fabrication Technology, 2020-2035

85. Australia Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

86. Australia Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

87. ASEAN Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

88. ASEAN Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

89. ASEAN Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

90. ASEAN Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

91. Rest of Asia Pacific Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

92. Rest of Asia Pacific Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

93. Rest of Asia Pacific Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

94. Rest of Asia Pacific Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

95. Latin America Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

96. Latin America Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

97. Latin America Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

98. Latin America Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

99. Mexico Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

100. Mexico Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

101. Mexico Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

102. Mexico Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

103. Brazil Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

104. Brazil Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

105. Brazil Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

106. Brazil Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

107. Argentina Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

108. Argentina Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

109. Argentina Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

110. Argentina Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

111. Rest of Latin America Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

112. Rest of Latin America Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

113. Rest of Latin America Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

114. Rest of Latin America Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

115. Middle East and Africa Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

116. Middle East and Africa Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

117. Middle East and Africa Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

118. Middle East and Africa Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

119. Saudi Arabia Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

120. Saudi Arabia Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

121. Saudi Arabia Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

122. Saudi Arabia Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

123. UAE Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

124. UAE Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

125. UAE Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

126. UAE Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

127. South Africa Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

128. South Africa Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

129. South Africa Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

130. South Africa Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

131. Rest of Middle East and Africa Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Grade, 2020-2035

132. Rest of Middle East and Africa Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Processing Method, 2020-2035

133. Rest of Middle East and Africa Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by Application, 2020-2035

134. Rest of Middle East and Africa Medical Polycarbonate Market Analysis and Forecasting (Tons) ($US Bn), by End-Use, 2020-2035

135. Competition Landscape

135.1. Market Share Analysis (%), by Company, 2024

135.2. Competitive Benchmarking

135.3. Company Profiles

135.3.1. Covestro AG

135.3.1.1. Company Overview

135.3.1.2. Product Portfolio

135.3.1.3. Financials

135.3.1.4. Geographical Footprint

135.3.1.5. SWOT Analysis

135.3.1.6. Recent Developments and Strategies

135.3.2. SABIC

135.3.2.1. Company Overview

135.3.2.2. Product Portfolio

135.3.2.3. Financials

135.3.2.4. Geographical Footprint

135.3.2.5. SWOT Analysis

135.3.2.6. Recent Developments and Strategies

135.3.3. Teijin Limited

135.3.3.1. Company Overview

135.3.3.2. Product Portfolio

135.3.3.3. Financials

135.3.3.4. Geographical Footprint

135.3.3.5. SWOT Analysis

135.3.3.6. Recent Developments and Strategies

135.3.4. Trinseo S.A.

135.3.4.1. Company Overview

135.3.4.2. Product Portfolio

135.3.4.3. Financials

135.3.4.4. Geographical Footprint

135.3.4.5. SWOT Analysis

135.3.4.6. Recent Developments and Strategies

135.3.5. Mitsubishi Chemical/Engineering-Plastics

135.3.5.1. Company Overview

135.3.5.2. Product Portfolio

135.3.5.3. Financials

135.3.5.4. Geographical Footprint

135.3.5.5. SWOT Analysis

135.3.5.6. Recent Developments and Strategies

135.3.6. Lotte Chemical

135.3.6.1. Company Overview

135.3.6.2. Product Portfolio

135.3.6.3. Financials

135.3.6.4. Geographical Footprint

135.3.6.5. SWOT Analysis

135.3.6.6. Recent Developments and Strategies

135.3.7. BASF

135.3.7.1. Company Overview

135.3.7.2. Product Portfolio

135.3.7.3. Financials

135.3.7.4. Geographical Footprint

135.3.7.5. SWOT Analysis

135.3.7.6. Recent Developments and Strategies

135.3.8. CHIMEI Corporation

135.3.8.1. Company Overview

135.3.8.2. Product Portfolio

135.3.8.3. Financials

135.3.8.4. Geographical Footprint

135.3.8.5. SWOT Analysis

135.3.8.6. Recent Developments and Strategies

135.3.9. Trinseo

135.3.9.1. Company Overview

135.3.9.2. Product Portfolio

135.3.9.3. Financials

135.3.9.4. Geographical Footprint

135.3.9.5. SWOT Analysis

135.3.9.6. Recent Developments and Strategies

135.3.10. Wanhua Chemical

135.3.10.1. Company Overview

135.3.10.2. Product Portfolio

135.3.10.3. Financials

135.3.10.4. Geographical Footprint

135.3.10.5. SWOT Analysis

135.3.10.6. Recent Developments and Strategies

135.3.11. Idemitsu Kosan

135.3.11.1. Company Overview

135.3.11.2. Product Portfolio

135.3.11.3. Financials

135.3.11.4. Geographical Footprint

135.3.11.5. SWOT Analysis

135.3.11.6. Recent Developments and Strategies

135.3.12. Eastman

135.3.12.1. Company Overview

135.3.12.2. Product Portfolio

135.3.12.3. Financials

135.3.12.4. Geographical Footprint

135.3.12.5. SWOT Analysis

135.3.12.6. Recent Developments and Strategies

135.3.13. GOEX Corporation

135.3.13.1. Company Overview

135.3.13.2. Product Portfolio

135.3.13.3. Financials

135.3.13.4. Geographical Footprint

135.3.13.5. SWOT Analysis

135.3.13.6. Recent Developments and Strategies

135.3.14. Luxi Chemical

135.3.14.1. Company Overview

135.3.14.2. Product Portfolio

135.3.14.3. Financials

135.3.14.4. Geographical Footprint

135.3.14.5. SWOT Analysis

135.3.14.6. Recent Developments and Strategies

135.3.15. RTP Company

135.3.15.1. Company Overview

135.3.15.2. Product Portfolio

135.3.15.3. Financials

135.3.15.4. Geographical Footprint

135.3.15.5. SWOT Analysis

135.3.15.6. Recent Developments and Strategies

135.3.16. Others

136. Appendix

- Get Started -

Get insights that lead to new growth opportunities

- Talk to Experts -

Get answers to your queries on this report from our experts

Frequently Asked Questions

The global medical polycarbonate market in 2024 was $US 1.6 billion.

The global medical polycarbonate market will be $US 3.3 billion by 2035.

The expected growth rate (CAGR%) of the global medical polycarbonate market is 6.9% for the period 2025-2035.

Growing Aging Populations Worldwide, Coupled with Rising Procedural Volumes, are Fueling Demand for Medical Devices, and Increase need for Sterilizable, Transparent, Durable Polymers and Regulatory Compliance.

The Hospitals & Clinics was the largest end-use segment in medical polycarbonate market in 2024.

North America was the leading regions for medical polycarbonate market holding around 38% of the global market in 2024.

Covestro AG, SABIC, Teijin Limited, Trinseo S.A., Mitsubishi Chemical/Engineering-Plastics, Lotte Chemical, BASF, CHIMEI Corporation, Trinseo, Wanhua Chemical, Idemitsu Kosan, Eastman, GOEX Corporation, Luxi Chemical, RTP Company, and others.